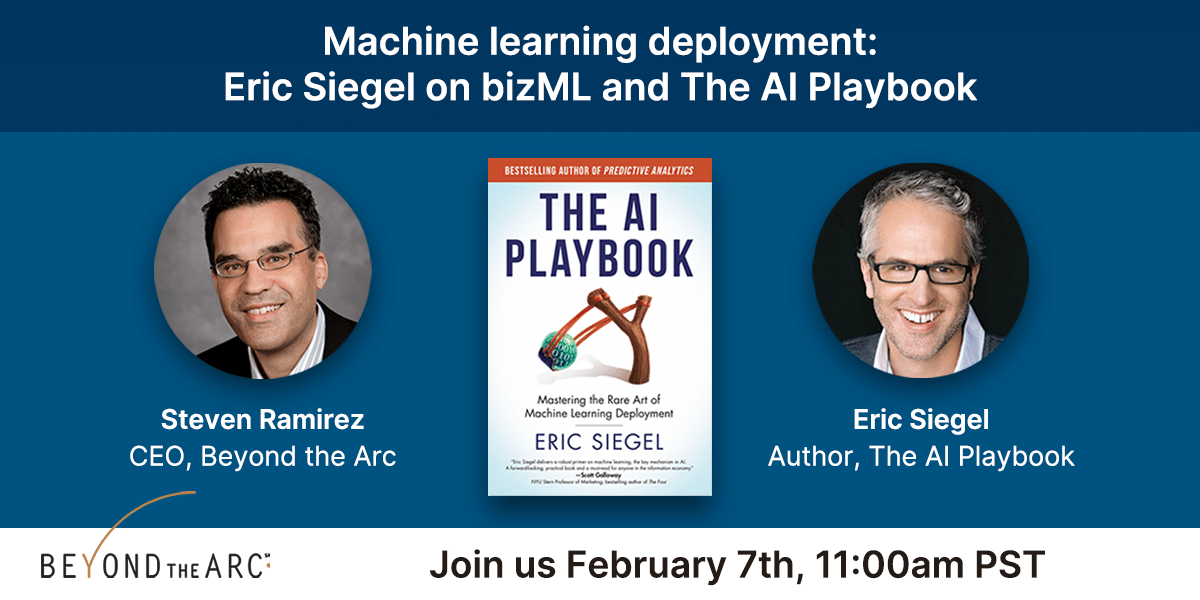

Machine learning deployment: Eric Siegel on bizML and The AI Playbook Gallery Machine learning deployment: Eric Siegel on bizML and The AI Playbook AI/ML, Data Analytics Machine learning deployment: Eric Siegel on bizML and The AI Playbook 2024-03-30T13:44:05-07:00By Steven Ramirez|AI/ML, Data Analytics| Read More

Generative AI Applications Summit And Machine Learning Week 2024: Shaping the Future with Community and Innovation Gallery Generative AI Applications Summit And Machine Learning Week 2024: Shaping the Future with Community and Innovation AI/ML Generative AI Applications Summit And Machine Learning Week 2024: Shaping the Future with Community and Innovation 2024-04-26T09:20:58-07:00By Beyond the Arc|AI/ML| Read More

AI as a business solution: beyond the tech hype Gallery AI as a business solution: beyond the tech hype AI/ML AI as a business solution: beyond the tech hype 2024-02-20T15:08:36-08:00By Beyond the Arc|AI/ML| Read More

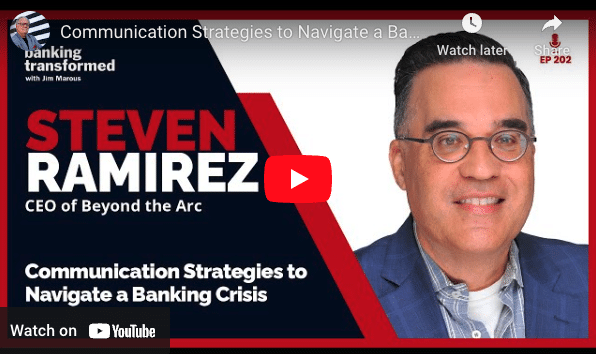

Crisis Communications Strategies – Banking Transformed podcast Gallery Crisis Communications Strategies – Banking Transformed podcast Communications, Customer Experience, Public Relations (PR) Crisis Communications Strategies – Banking Transformed podcast 2024-01-16T11:46:55-08:00By Beyond the Arc|Communications, Customer Experience, Public Relations (PR)| Read More

Emotional Intelligence in AI: prompt engineering best practices Gallery Emotional Intelligence in AI: prompt engineering best practices AI/ML, Best Practices Emotional Intelligence in AI: prompt engineering best practices 2024-02-09T09:23:45-08:00By Beyond the Arc|AI/ML, Best Practices| Read More

PODCAST: Getting ready for the largest wealth transfer ever Gallery PODCAST: Getting ready for the largest wealth transfer ever Customer Experience, Data Analytics, FinTech, Marketing, Uncategorized, Wealth Management PODCAST: Getting ready for the largest wealth transfer ever 2023-07-20T14:40:42-07:00By Beyond the Arc|Customer Experience, Data Analytics, FinTech, Marketing, Uncategorized, Wealth Management| Read More

5 Tips for connecting with customers through empathy Gallery 5 Tips for connecting with customers through empathy Best Practices, Communications, Customer Experience 5 Tips for connecting with customers through empathy 2024-02-09T09:48:48-08:00By Beyond the Arc|Best Practices, Communications, Customer Experience| Read More

Hiring a fintech content writer: Go beyond the checklist Gallery Hiring a fintech content writer: Go beyond the checklist Communications, FinTech Hiring a fintech content writer: Go beyond the checklist 2023-04-26T17:55:58-07:00By Beyond the Arc|Communications, FinTech| Read More

2023 Trends in CX, Fintech & AI: Go bold or get left behind Gallery 2023 Trends in CX, Fintech & AI: Go bold or get left behind AI/ML, Customer Experience, FinTech, Social Media 2023 Trends in CX, Fintech & AI: Go bold or get left behind 2024-01-06T17:26:52-08:00By Beyond the Arc|AI/ML, Customer Experience, FinTech, Social Media| Read More

3 top ways to communicate better with customers Gallery 3 top ways to communicate better with customers Communications, Customer Experience 3 top ways to communicate better with customers 2024-02-09T13:33:12-08:00By Beyond the Arc|Communications, Customer Experience| Read More

How healthcare IoT can transform efficiency and patient experience Gallery How healthcare IoT can transform efficiency and patient experience Customer Experience, Internet of Things (IoT) How healthcare IoT can transform efficiency and patient experience 2022-12-15T17:46:24-08:00By Gavin James|Customer Experience, Internet of Things (IoT)| Read More

Make your marketing pivot with a fintech content agency Gallery Make your marketing pivot with a fintech content agency Communications, FinTech Make your marketing pivot with a fintech content agency 2024-04-13T20:08:32-07:00By Steven Ramirez|Communications, FinTech| Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}